Blockchain in a nutshell

In Brief

- What is blockchain technology? What does a blockchain look like How many copies of a blockchain are there? The relationship between nodes and cybersecurity.

- How does blockchain work? How is data added to a blockchain? How are blocks added to a blockchain? Example of how a bitcoin transaction takes place.

- Use cases for blockchain technology beyond the financial sector

Blockchain, like Artificial Intelligence, appears in any conversation about technology, the future of payments, and even new forms of cyber security. But while the applications of blockchain technology seem endless, few people are sure what it is.

That’s what we’re going to cover in this article.

1 — What is Blockchain technology?

Blockchain technology eliminates the need for a trusted party to facilitate digital relationships and is the backbone of cryptocurrencies. Blockchain is a type of accounting technology that stores and records data.

In the past, transactions were tracked in written ledgers and stored in financial institutions. Traditional ledgers could be audited, but only by those with privileged access.

Well, blockchain technology has taken these concepts and democratized them, removing the secrecy about how information — i.e. transaction data — was handled.

Put more simply, a blockchain is a distributed list of transactions that is constantly updated and revised.

As an evolution of Distributed Ledger Technologies (DLTs), it can be programmed to record and track anything of value in a network “spread out” (distributed) across multiple locations and entities. And this creates a kind of worldwide web of interconnected computers.

Although blockchain technology emerged with Bitcoin in 2008, blockchain technology has also been applied in a number of areas beyond the cryptoassets market. Thanks to its unique ability to add and record data, it can serve many other functions in various sectors, such as healthcare, real estate, energy, voting, supply chain, music, streaming, Web3 and many others.

2 — What does a blockchain look like?

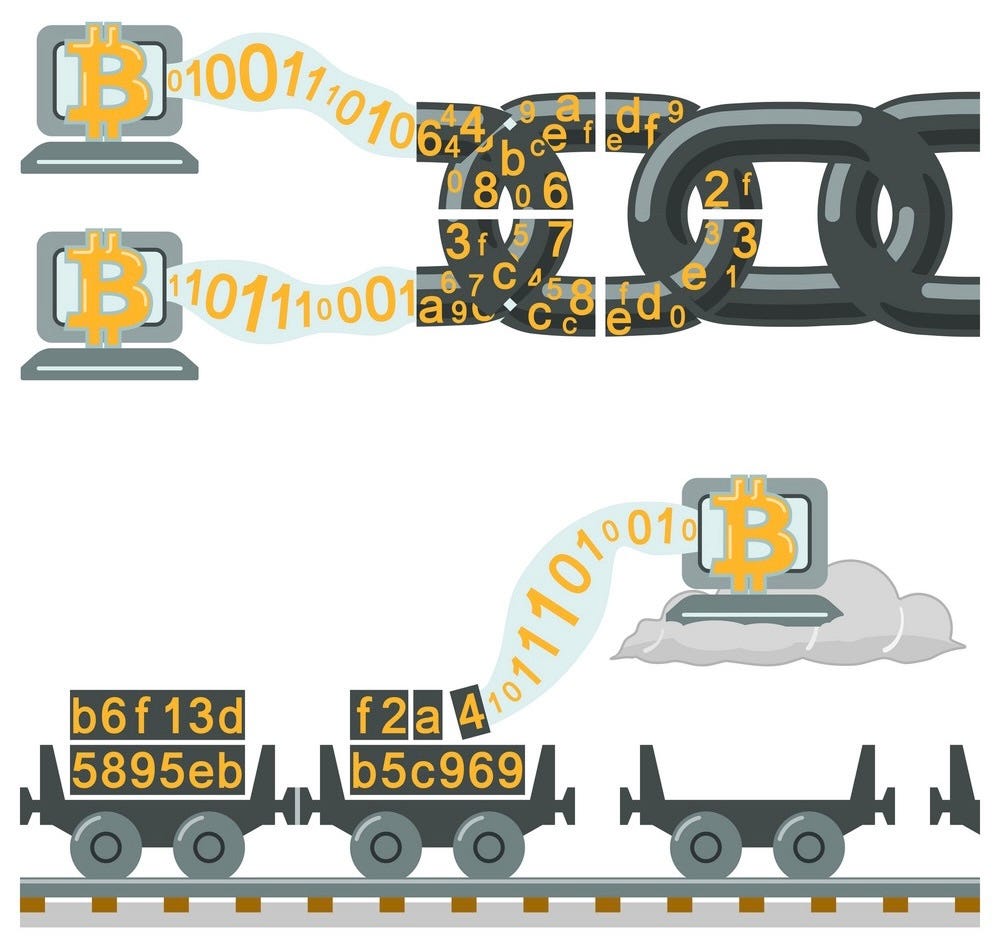

A blockchain can be divided into two components: the block and the chain.

A block is a collection of data linked to other blocks chronologically in a virtual chain.

You can think of a blockchain as a train consisting of several wagons connected on a track, where each wagon contains a quantity of data.

Just as with the passengers in a real-life train carriage, the blocks can only accommodate a certain amount of data before they become full.

Each block also contains a timestamp, so it is clear when the data was recorded and stored — something that is vital for data such as transactions or the supply chain, where it is important to know exactly when a payment or package was processed.

3 — How many copies of a Blockchain exist?

There is no single master copy of a blockchain.

Instead, each person who manages a computer that contributes to the network — also known as a “node” — maintains their own copy of the blockchain and constantly checks with other nodes to ensure that they all have the same data record.

Having each individual employee store their own copy means that there is no single point of failure.

This impressive layer of security also means that it is virtually impossible for malicious agents to tamper with the data stored on blockchains.

4 — The link between nodes and cybersecurity

If a group of hackers wanted to manipulate any transaction on a blockchain, they would have to hack into the device of every network collaborator around the world and alter all the records to show the same thing.

Unlike a database of financial records stored by traditional institutions, the blockchain is completely transparent and is intended to be distributed, shared between networks and, in many cases, completely public. By prioritizing transparency around transactions and how information is stored, blockchain can act as a single source of truth.

To find out more about cybersecurity in blockchains, see here.

5 — How does blockchain work?

In general terms, the two main components of blockchains are the blocks of information and the infinite virtual chain that connects and tracks this information.

Here are some additional key terms to understand:

- Block — a collection of data that contains a timestamp and other encrypted information about recent transactions that needs to be validated by the network before being added to the network.

- Nodes — the computers in a network that keep complete copies of all transactions, making it virtually impossible to tamper with them.

- Hash — an alphanumeric sequence that confirms transactions on the blockchain and serves as a digital stamp.

- Mining — the process of verifying and adding blocks to a blockchain ledger, as well as creating new cryptocurrencies using a proof-of-work (PoW) consensus mechanism. Understand in detail what mining is here.

- Nonce — short for “number used only once”, is an encrypted number that miners need to solve to verify a new block on the blockchain before “sealing” it.

- Distributed ledger — a set of data records that is shared and synchronized between members of a decentralized network.

- Block reward — the incentive mechanism obtained by miners that is used to encourage participation in the network.

There are several long-standing technologies that work together to power a blockchain.

Cryptography refers to protecting information by transforming it so that only the intended recipient can process it. Blockchain uses two types of cryptographic keys — a public key and a private key — to create a secure digital identity.

A distributed network is then used to validate transactions and keep the network secure. The whole process is governed by a single set of rules called a Protocol.

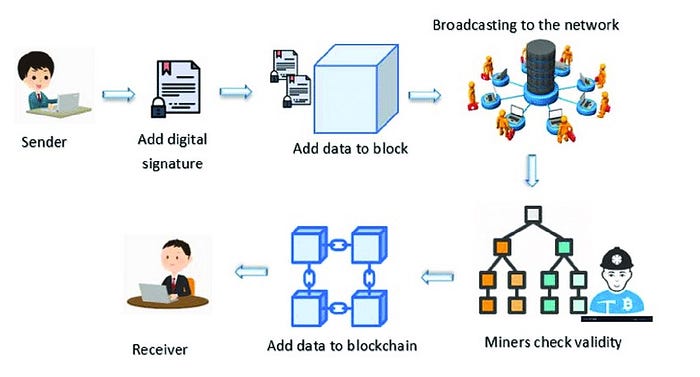

4 — How are data added to a blockchain?

As well as being transparent with data, blockchain is also a secure way of storing it. Using Bitcoin as an example, see how a transaction is added to a new block:

- When a bitcoin user sends a transaction to the Bitcoin blockchain, a message is created with the public addresses of the sender and recipient and the amount being transacted.

- The sender takes this data, adds their private key to the message and then hashes it (turns it into a fixed-length code).

- This creates a digital signature to confirm that the person who owns a certain amount of bitcoin intends to send it to the recipient.

- The sender then packages this digital signature with the message and its own public key and transmits it to the network. It’s like saying: “Hey guys! I want to send bitcoin to this person.” For most wallets and other applications, all this happens “behind the scenes” and users don’t actually have to deal with the processes themselves.

- The packaged transaction enters a waiting room full of other unconfirmed transactions that want to be added to the blockchain, known as the “mempool”.

In the case of the Bitcoin network, miners who have been authorized to validate new blocks — by solving the mathematical problem created by the Proof of Work consensus algorithm — take a batch of transactions from the mempool (usually based on which ones have the highest fees attached), verify each transaction to ensure that each sender really does have the amount of bitcoins in their wallets that they want to send, run them through software to ensure that the packaged data — digital signatures, messages and public keys — are legitimate, add them to the new block and finally transmit the proposed new block to the network so that other miners can check that everything is correct.

This is similar to the process used in proof-of-stake blockchains (PoS), except that instead of mining nodes discovering and verifying transactions, users who have blocked an amount of cryptocurrency — known as “stakers” or “validators” — carry out the process.

Nodes can perform a variety of tasks. This includes keeping a historical record of all transaction data — what is known as a full node — verifying transactions and, in the case of mining nodes or validator nodes, adding new blocks to the blockchain network.

Once a transaction has been approved and added, the information cannot be changed or rewritten. This is why the data recorded on a blockchain network is described as “immutable”.

The blockchain simply records all the transactions that have ever taken place on its network. The Ethereum blockchain is, for example, a record of all the ether transactions that have ever taken place.

Therefore, if there are updates that need to be made around a previous transaction, instead of deleting and rewriting some data already recorded on the network, a new record is made, informing you of the change.

How are blocks added to a blockchain?

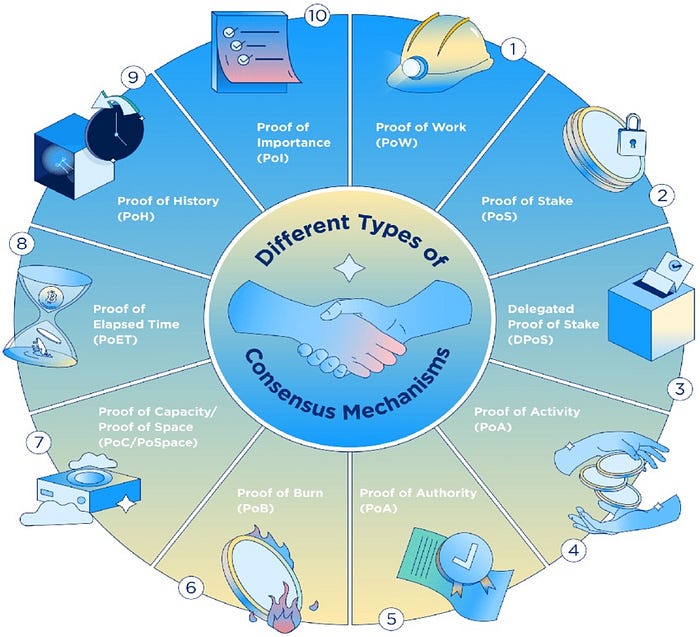

There are different consensus mechanisms used to verify transactions and add new blocks to a blockchain.

The most common consensus mechanisms are proof of work (PoW) and proof of stake (PoS). But there are many others, as we can see in the figure below.

Bitcoin was introduced in Satoshi Nakamoto’s 2008 article entitled “Bitcoin: A Peer-to-Peer Electronic Cash System” and was the first major application of blockchain technology. It uses a proof-of-work consensus method to create new blocks and put new bitcoins into circulation. This method verifies transactions through mining, and the users who verify transactions are known as miners.

As there is no central authority, transactions are managed and new coins are issued collectively by the network.

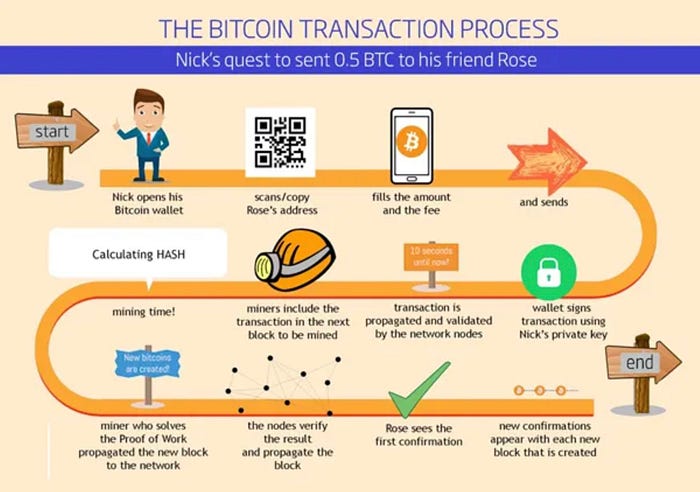

Here is an example of how a bitcoin transaction would take place:

1. Nick opens his bitcoin wallet. With this, Nick indirectly creates his own bitcoin address.

2. Imagine that he receives some bitcoins, and wants to transfer 0.5 bitcoin to his friend Rose.

3. To do this, he scans or copies Rose’s bitcoin address.

4. Next, Nick fills in the amount of bitcoins he wants to transfer to Rose (0.5 btc) and the fee he is willing to pay for this transaction. A transaction therefore includes inputs, outputs and the amount of bitcoins that will be transferred.

5. Before sending the new transaction to the blockchain, the wallet uses Nick’s private key to sign the transaction.

6. The transaction is then transmitted to the nearest node in the bitcoin network. It is then propagated on the network and checked — for example, whether there are enough bitcoins in the source wallet, structure, etc.). After passing this initial check, the information goes to the “Mempool” (short for Memory Pool) and waits patiently until a miner picks up this transaction to record it in the next block to be mined.

7. Next, the miners collect the transactions (first the ones that pay the highest transaction fees) and group them into blocks, trying to solve the Proof of Work (or POW — a consensus algorithm) and calculate a certain hash function.

8. The miner who obtains the result wins the right to include the new block in the blockchain network.

9. The nodes verify the result and propagate the new block to all the nodes on the network, which must verify and agree that the block is valid before adding it to the official chain. The average time taken to confirm a bitcoin transaction is around 10 minutes.

10. At that time, Rose sees the first confirmation of the transaction. New confirmations appear with each new block that is created and linked.

When the process is complete, Rose will have received 0.5 BTC sent to her by Nick, all the nodes on the network will have agreed to the transaction using the chosen consensus model and a bitcoin miner will have earned a reward for verifying a successful transaction.

The new block containing this transaction is now linked to other blocks on the blockchain network as part of an infinite, public chain.

Today, there are thousands of cryptocurrencies running on dozens of blockchain networks.

Blockchain networks such as Ethereum and Bitcoin continue to upgrade their networks, integrating new ways to become more efficient, energy-conscious and cheaper than ever before.

But beyond its use in cryptocurrencies, blockchain technology is also used in use cases that go beyond financial transactions.

6 — Other use cases of blockchain technology

Blockchain eliminates or reduces the need for intermediaries such as corporations and financial institutions. The peer-to-peer (P2P) network eliminates/reduces intermediaries and allows for more secure, low-cost transactions that can be reviewed by anyone.

As well as being used in the financial sector, blockchain technology has many other functions. Hospitals are integrating blockchain to help track medical record data and improve its accuracy. Agricultural companies use blockchain to track the food supply chain.

Smart contracts rely on blockchain technology to keep track of all agreements and changes of state.

More recently, blockchain has become a means of trading, selling and authenticating original pieces of digital art, concert tickets and music.

In this context, blockchains are becoming an increasingly important part of how we live, work and interact with our digital information.

As with any revolutionary new technology, there is still no prediction of all the benefits and the size of the global impact that blockchain technology can bring.

The only certainty here is that blockchain technology is here to stay.